Payments are the part of running a dating site that operators discover the hard way. The technology is straightforward; the problem is that the payments industry treats dating with suspicion. This guide explains how dating payment systems work, why they are harder than they look, and how changes the picture.

What a dating payment system must do

A dating site payment system is more than a checkout button. It has several jobs that all have to work together.

It must acquire payments, which means having a merchant account and the ability to take card payments and, increasingly, alternative methods. It must handle subscriptions, since most dating sites bill recurring memberships, which means managing renewals, failed payments, upgrades and cancellations. It must tokenise payment data, so that card details are stored and reused securely without the operator holding raw card numbers. It must collect tax correctly across the jurisdictions where members pay. And it must handle chargebacks and refunds, which in dating is a continuous operational task rather than an occasional one.

Each of these is a real piece of work, and together they make payment processing one of the genuinely hard parts of running a dating site, harder, usually, than the dating product itself.

Why dating is treated as high risk

The single most important thing to understand about dating payments is that the payments industry does not treat dating like an ordinary online business. It classifies dating as elevated or high risk.

There are reasons for this classification. Dating has historically had higher-than-average rates. It involves recurring billing, which generates disputes. Parts of the sector sit close to adult content, which carries its own scrutiny. And card networks watch the category closely. None of this means dating is illegitimate; it is a large, mainstream, legal industry. But it does mean payment providers price and gate it differently.

The practical consequence is severe and surprises operators: many mainstream payment processors will simply not serve a dating site, or will serve it and then withdraw. An operator who assumes the familiar everyday payment providers are available, builds the business on that assumption, and then finds the account declined or closed, has a serious problem. The high-risk classification is the fact that shapes every other payment decision.

Choosing a payment service provider

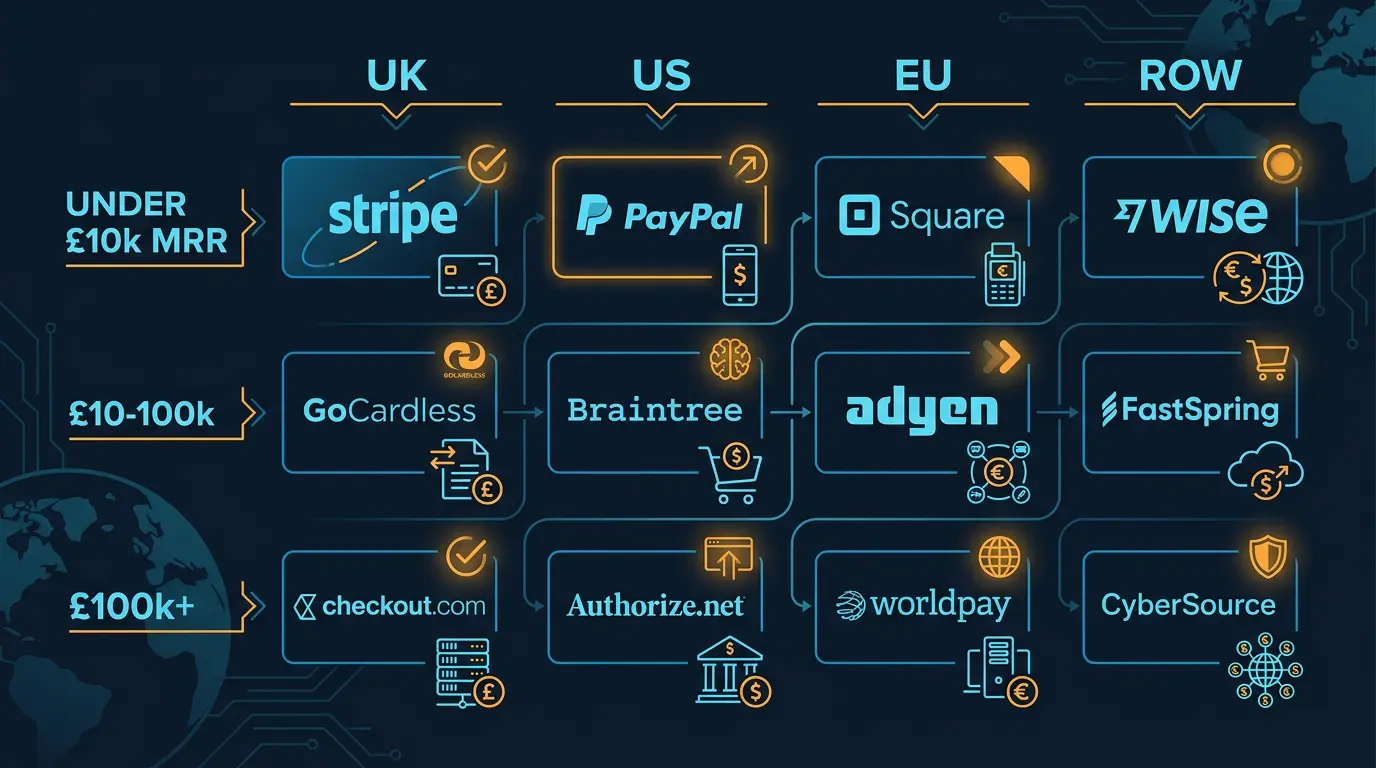

Because of the high-risk classification, choosing a payment service provider, a PSP, is a deliberate exercise, not a default.

You need a PSP that genuinely accepts dating businesses. There are processors and PSPs that specialise in, or are comfortable with, dating and other elevated-risk categories. These are the ones to look at. The mainstream, consumer-familiar processors may or may not accept dating, and may accept mainstream dating while refusing anything casual or adult-adjacent.

When assessing a PSP for a dating site, check several things: that they explicitly accept dating, and your specific type of dating; their fees, which for high-risk categories are typically higher than standard; their chargeback policies and the thresholds at which they take action; their settlement terms; their support for subscription billing; and their stability and reputation, because a PSP that suddenly drops your account is a genuine business risk. Expect higher fees and stricter terms than an ordinary online business would face, and budget for them.

Subscription and recurring billing

Most dating sites are subscription businesses, so recurring billing is central, and it carries its own demands.

A subscription system must manage the full lifecycle: initial signup, recurring renewals, upgrades and downgrades, plan changes, and cancellations. It must handle failed payments gracefully through a process called dunning, retrying payments and prompting members to update expired cards, because a meaningful share of subscription revenue is lost simply to cards expiring rather than to members choosing to leave.

Recurring billing also generates disputes, which feeds the chargeback problem below. Clear communication with members about what they are subscribed to, when they will be billed, and how to cancel, reduces disputes and is also, increasingly, a regulatory expectation around subscription transparency. A well-run subscription system is not just a technical component; it is a meaningful lever on revenue, because better dunning and clearer communication directly protect the recurring income the whole business depends on.

Credit and one-off payment models

Not every dating site uses pure subscriptions. Some use a credit model, where members buy credits or tokens and spend them on contact, visibility or features, and some use a hybrid.

Credit models suit a more transactional intent, which is why they appear often in casual dating, and they change the payment picture: more one-off purchases, fewer recurring renewals, a different dispute pattern. A payment system supporting credits must handle the purchase, the balance, and the spending of credits cleanly.

Whichever model a site uses, the underlying payment realities, the high-risk classification, the need for a dating-friendly PSP, the chargeback exposure, the tax obligations, all still apply. The model changes the mix of transactions, not the fundamental challenge of getting dating payments processed reliably.

Chargebacks, the dating site's constant battle

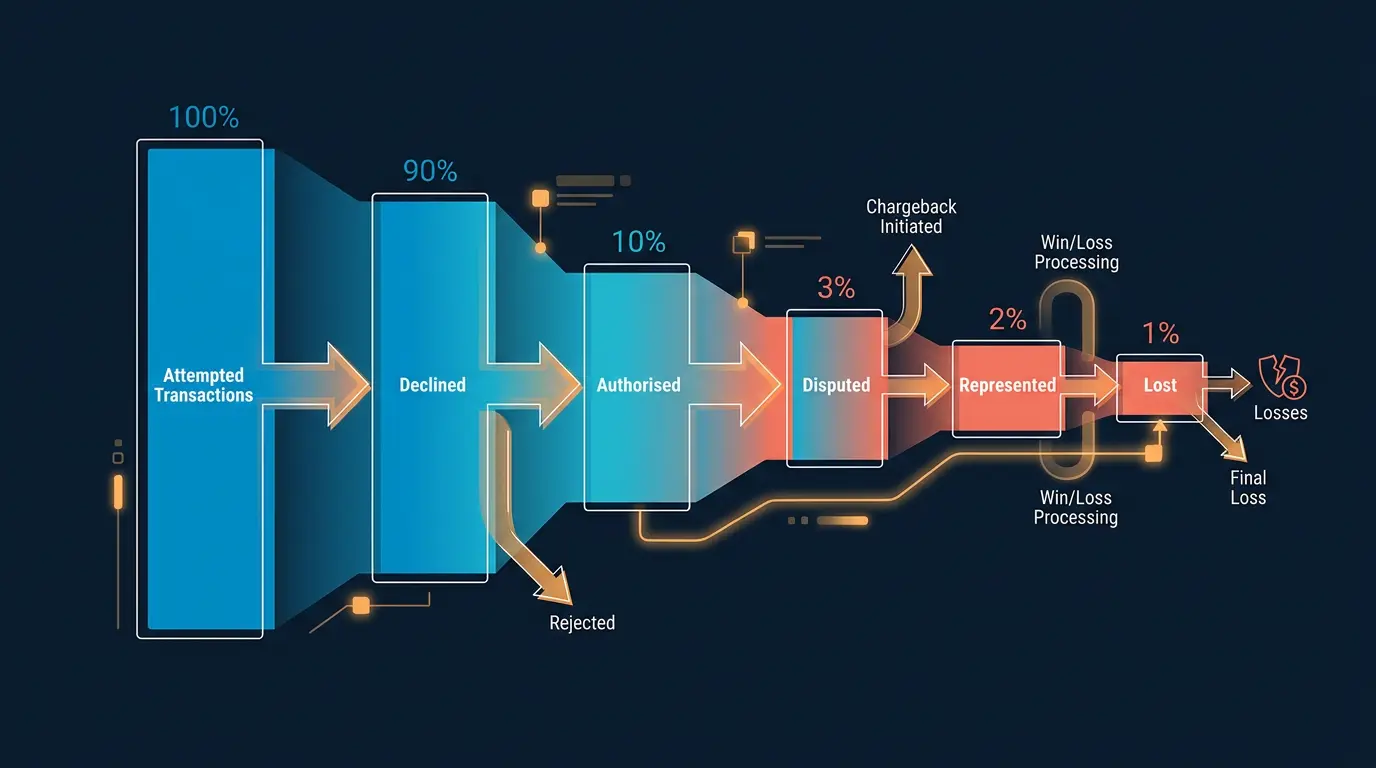

Chargebacks deserve their own section because, in dating, they are not an occasional nuisance but a continuous operational reality.

A chargeback happens when a member disputes a payment with their card issuer rather than seeking a refund from the site. Dating runs a higher chargeback rate than most online categories, for several reasons: recurring billing generates disputes, some members dispute charges they recognise but regret, and a portion of chargebacks are effectively a way of getting a refund. Card networks monitor chargeback rates closely, and a site or processor that exceeds certain thresholds faces penalties or loss of processing.

Managing chargebacks is therefore a permanent task: clear billing descriptors so members recognise the charge, transparent subscription terms and easy cancellation so members refund rather than dispute, responsive support, fraud screening to stop bad transactions before they happen, and disputing illegitimate chargebacks with evidence. For an operator, the contractual question of who absorbs the chargeback loss, the operator's revenue share or the provider, is one of the most important terms in any dating platform agreement.

Tax across jurisdictions

A dating site with members in different countries collects payments across tax jurisdictions, and tax is a genuine, ongoing obligation that operators underestimate.

Digital services and subscriptions are subject to consumption taxes that vary by country: VAT in the UK and EU, sales tax across US states, and a growing number of digital services taxes elsewhere. The rules around which jurisdiction's tax applies, and at what rate, are detailed, and they change.

A dating payment system must calculate, collect and account for the correct tax for each member's location. This is complex enough that it is a real reason to value a payment setup, or a white label provider, that handles tax properly. Getting tax wrong is not a minor error; it is a compliance failure with financial consequences. An operator running their own payment system must take tax seriously and may need specialist help. An operator on white label should confirm exactly how tax is handled.

Payment fraud and security

Payment fraud and payment security are the final pieces of the picture.

On security, any system handling card payments must comply with , the card industry's data security standard, and should tokenise card data so raw card numbers are never stored insecurely. This is mandatory, not optional.

On fraud, dating attracts payment fraud, including stolen-card use, which both causes losses and drives up chargebacks. A dating payment system needs fraud screening that can flag and block suspicious transactions before they complete. Effective fraud prevention also protects the chargeback rate, which protects the ability to process payments at all.

Payment security and fraud prevention are specialised work. They are a strong argument for either a capable, dating-experienced PSP or a white label provider whose payment stack already includes them, because an operator building this alone is taking on a demanding, high-stakes responsibility.

Alternative payment methods and global members

Most discussion of dating payments assumes the card, but a dating site with members in different countries quickly finds that the card is not universal, and how a payment system handles that affects real revenue.

In some markets card payments dominate and nothing else is needed. In many others they do not. Digital wallets are the normal way to pay in large parts of the world. Some countries rely heavily on local bank-transfer schemes, or on payment methods that have no equivalent elsewhere. A member who wants to subscribe but is not offered a payment method they actually use will simply not subscribe, and the operator never sees that lost revenue as anything other than a slightly lower conversion rate.

So for a dating site with any international ambition, supporting payment methods beyond the card is not a refinement; it is a way of not turning away willing members. The practical question is which methods matter for the specific markets a site serves, because supporting every method everywhere is neither possible nor sensible. A site whose members are concentrated in one or two countries needs the methods those countries use; a site spread more widely needs a broader set.

There is also the related issue of currency. Members generally prefer, and convert better when, prices are shown and charged in their own currency rather than a foreign one. A payment system that presents local pricing removes a small but real piece of friction at exactly the moment a member is deciding whether to pay.

For an operator running their own payment system, this means choosing a payment service provider that supports the methods and currencies the target markets need, which is one more criterion in an already demanding PSP selection. For a white label operator, it is one more thing to confirm: ask which payment methods and currencies the provider's payment stack supports, and check that they cover the markets the site is aiming at. Payment methods that fit the member, rather than only the operator's home market, quietly protect conversion.

What white label handles for you

For an operator on a white label platform, almost everything in this guide is the provider's job, and that is one of white label's most valuable features.

On a typical white label platform, the provider is the merchant of record. They hold the merchant account, they have solved the high-risk PSP problem, they run the subscription billing and dunning, they tokenise card data and maintain PCI DSS compliance, they handle tax collection across jurisdictions, and they run payment fraud screening. The operator simply earns a revenue share of the payments the provider processes.

This removes what is, for an independent operator, one of the single hardest parts of running a dating site. The one thing the operator must still do is read the contract carefully, because how chargebacks are allocated, what the revenue share is calculated on, and how refunds affect the operator's earnings are all defined there. White label solves the payment problem, but the commercial terms around it are still yours to scrutinise.

What to confirm before you launch

Whichever route you take, confirm the payment picture before you launch, not after.

If you are running your own payment system, confirm you have a PSP that genuinely and durably accepts your type of dating site, understand the fees and chargeback thresholds, have a plan for subscription billing and dunning, have addressed tax across your markets, and have PCI DSS compliance and fraud screening in place.

If you are on white label, confirm that the provider's payment processing genuinely covers your type of dating site, including casual or adult-adjacent if relevant, and read the contract for the chargeback allocation, the revenue share basis, and the refund handling.

Payments are the area most likely to delay or derail a launch, because the high-risk classification can turn what looks like a formality into a weeks-long problem. Start the payment conversation early.

Common mistakes

The defining mistake is assuming mainstream payment processors will serve a dating site. Many will not, and an operator who builds on that assumption can find the account declined or closed.

The second is underestimating chargebacks, treating them as occasional rather than as a continuous operational battle that must be actively managed.

The third is ignoring tax across jurisdictions, which is a genuine compliance obligation with financial consequences.

The fourth is leaving payment setup until late, when the high-risk classification can make it a slow, launch-delaying problem. The fifth, for white label operators, is signing the contract without reading exactly how chargebacks and the revenue share work. Treat payments as a serious, early priority, not an afterthought.

What to read next

For the chargeback angle in depth, read how to handle chargebacks on a dating site and chargeback fraud prevention. For payment security, see PCI DSS for dating sites. And to understand how a white label provider handles payments end to end, DatingPartners.com can walk through its payment stack.

DatingPartners integrates Segpay, CCBill and Stripe with chargeback tooling baked in. Skip the approvals drama.

Visit DatingPartners.com →